Capacity Market auctions clear at £20/kW for 2025-26 and £60/kW for 2028-29

The Electricity Market Reform (EMR) Delivery Body has made announcements regarding the T-1 and T-4 Capacity Market (CM) auctions for delivery years 2025-26 and 2028-29 respectively.

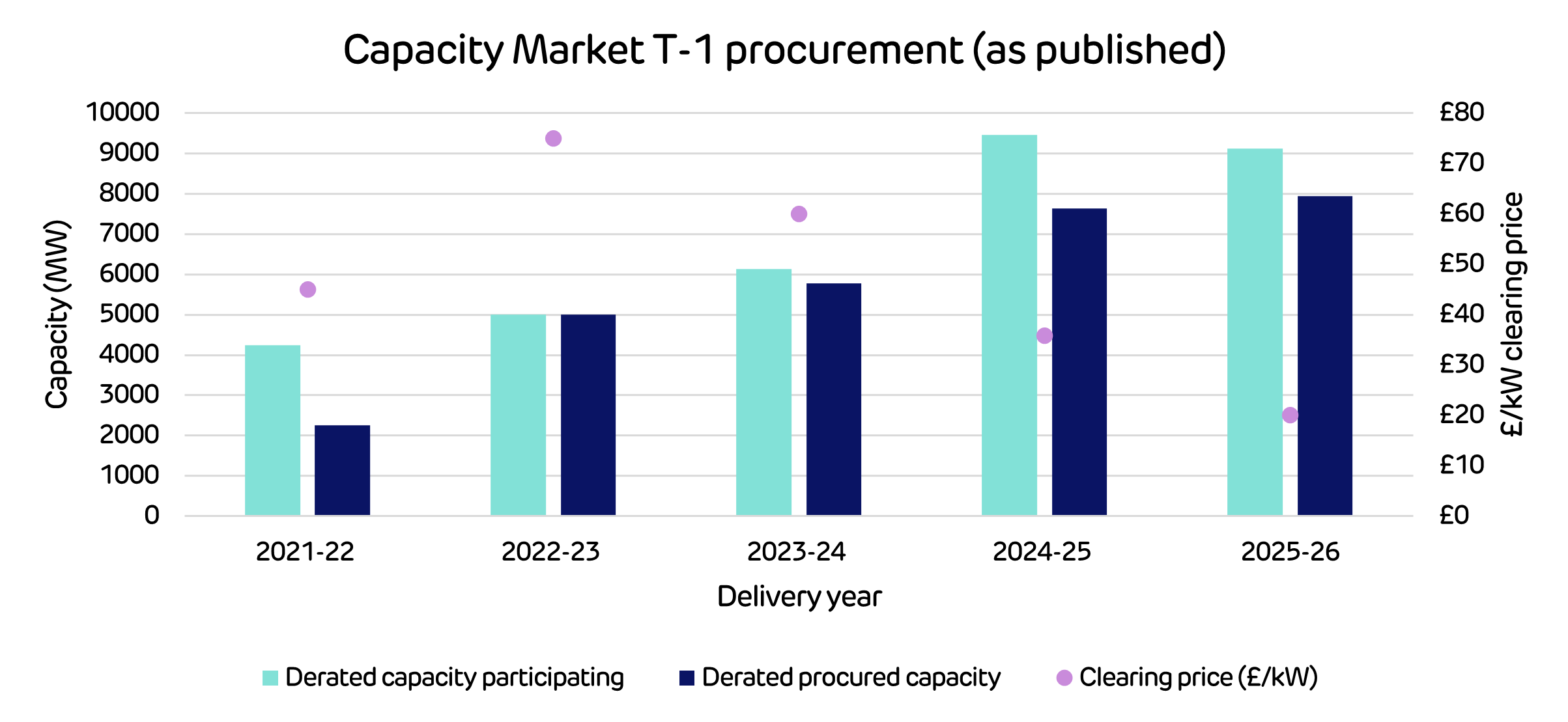

- The T-1 auction cleared at £20.00/kW, with 7.94GW of de-rated capacity receiving an agreement procured across 246 Capacity Market Units (CMUs).

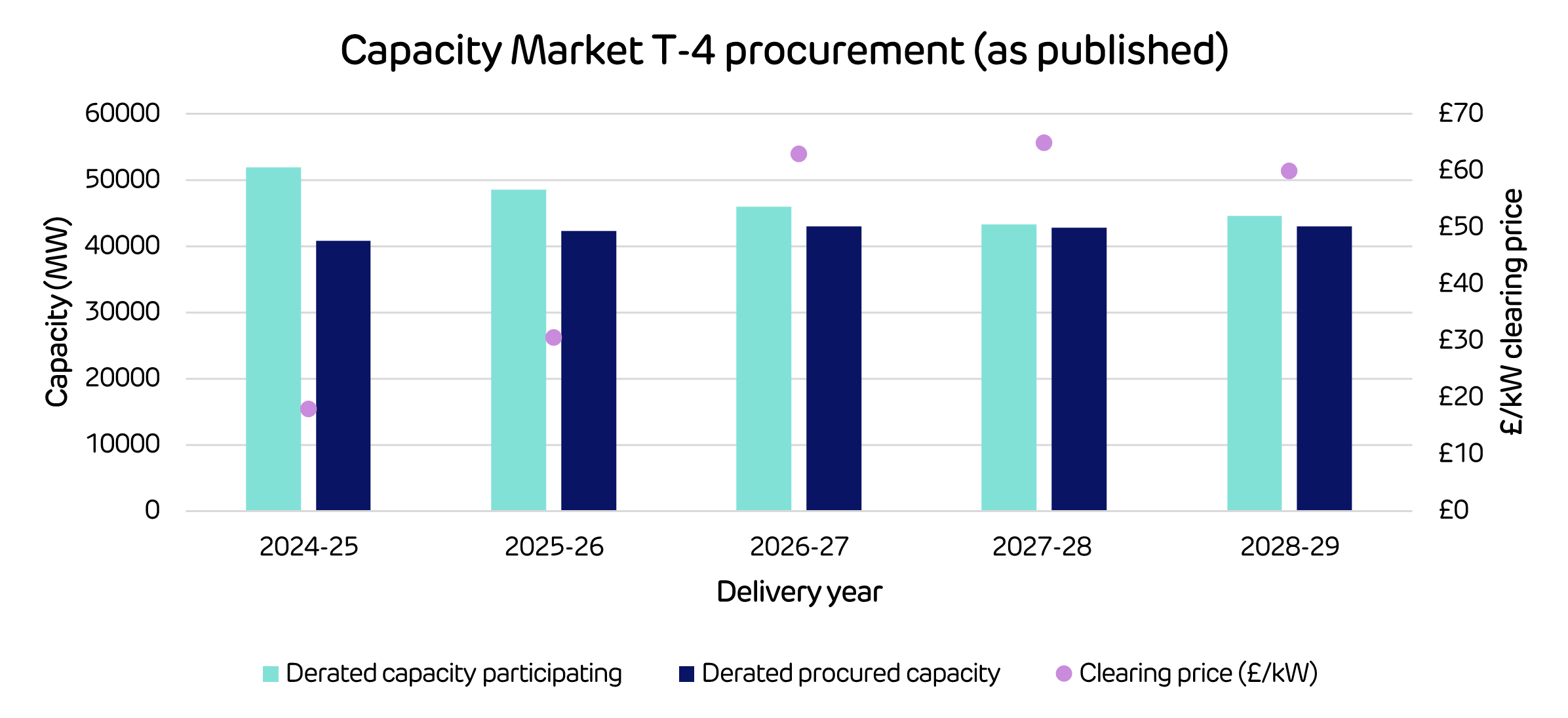

- The T-4 2028/29 auction cleared at £60.00/kW, with 43.06GW of de-rated capacity receiving an agreement across 669 CMUs.

Both clearing prices are lower than the auctions held in the previous year. However, this is the third year in a row that the T-4 CM auction has cleared at or above £60/kW.

The T-1 auction exceeded its target capacity by 436.29MW. Over 75% of the cleared capacity comprised existing generation or proven demand-side response (DSR). Unproven DSR comprised 6% of awarded capacity, while 9% was awarded to New Build Generating CMUs.

The chart below explores the de-rated capacity participating and the de-rated capacity procured in each T-1 auction, alongside the published clearing price. Clearing prices have declined over the past few years, with higher levels of de-rated capacity participating, and lowering concerns about winter peak margin since the Russian invasion of Ukraine.

96% of capacity entering the T-4 auction received an agreement, as did most of the existing capacity in the T-4 auction (a small number of combined heat and power – CHP – plants were the exceptions). 81% of the capacity awarded an agreement was either existing or proven DSR.

A record number of Battery Energy Storage Systems (BESS) and DSR were successful in the auction, including a wide range of 1-hour to 8.5-hour storage, with the modal 2-hour duration. The chart below explores the de-rated capacity participating and the de-rated capacity procured in each T-4 auction, alongside the published clearing price.

The annual cost for delivery year 2025-26 from the recent T-1 auction and the previous T-4 auction in 2021-22 is £1.45bn (excluding prior multi-year contracts and inflationary adjustment). Despite a lower clearing price in the T-1 auction, this is a 44% increase from the year before, due to the substantial uplift in the T-4 clearing price (£12.59/kW).

Consumers can also expect to see further increases in the future delivery years, driven by substantial uplifts to T-4 clearing prices (see the chart above).

See our Electricity Prices Explained Summary Guide for an overview of Third Party Charge drivers.

Disclaimer

We’ve used all reasonable efforts to ensure that the content in this article is accurate, current, and complete at the date of publication. However, we make no express or implied representations or warranties regarding its accuracy, currency or completeness. We cannot accept any responsibility (to the extent permitted by law) for any loss arising directly or indirectly from the use of any content in this article, or any action taken in relying upon it.