Tariffs, trade, storage and ceasefire: volatility dominates the energy markets

This winter, energy prices started the season lower than we’ve seen since the Russian invasion of Ukraine in February 2022. Europe’s economic response in the immediate aftermath was to cut Russian gas imports, which led to a surge in prices. Winter months were particularly influenced due to the seasonal peak driven by higher demand in colder weather. This year, winter started with strong storage levels and shifting demand patterns. Having mostly adjusted to an environment without Russian pipeline gas, Europe has diversified its supply routes and sources. Despite these readjustments, there have been many uncertainties influencing the energy market, driving greater volatility over the recent winter months.

Recent trends

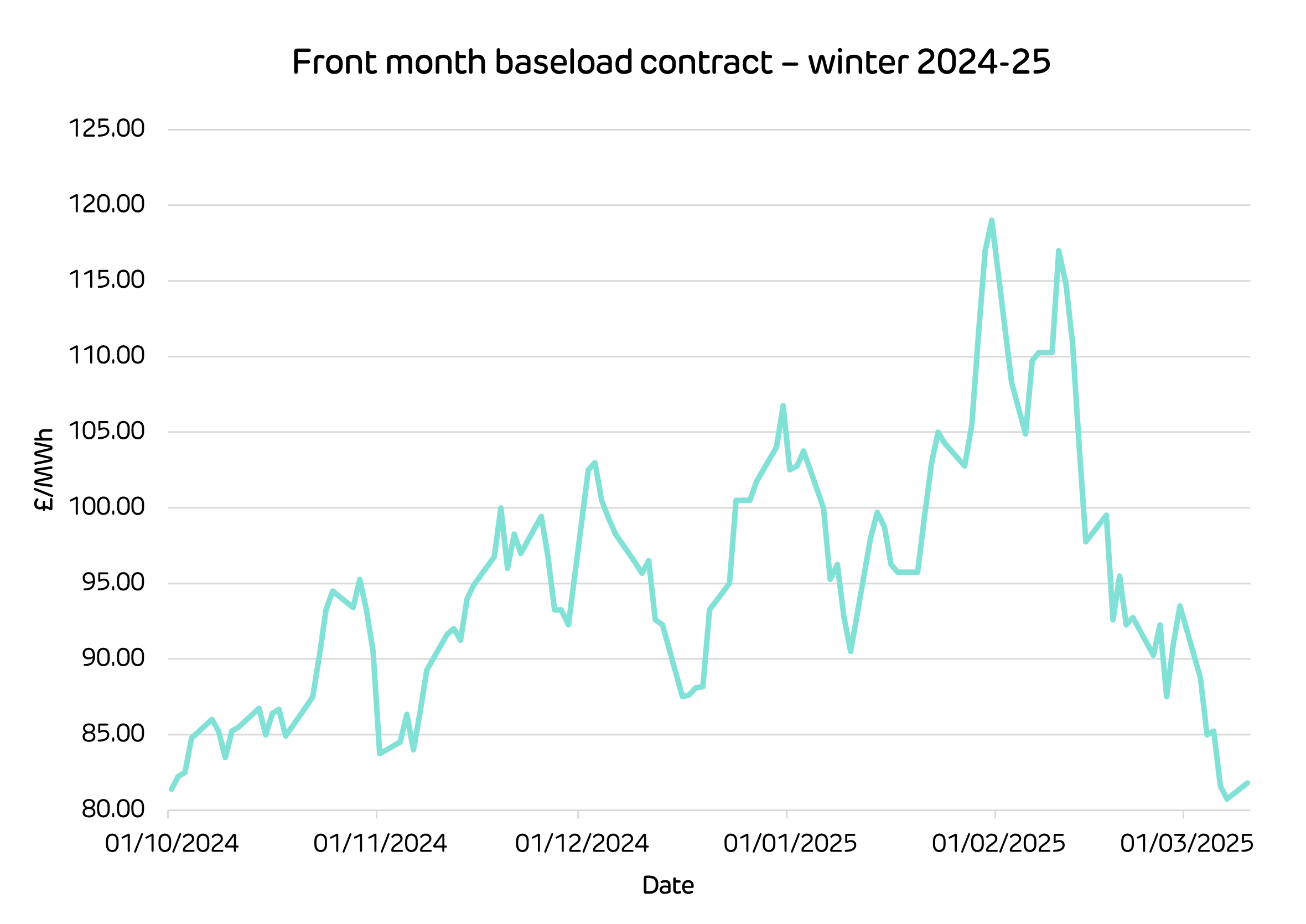

The following graph outlines the month ahead baseload contract over time, starting with the winter contract spanning 1 October 2024 to mid-March 2025.

Despite EU gas storage reserves reaching 95% by mid-October, the rapid depletion of stocks throughout the winter months has provided a buoyant influence on prices. This was a result of several cold snaps, especially significant when experienced alongside spells of high pressure and still conditions, which lower renewable generation. The lead up to January 2025 also saw prices climb, given the need for renegotiation of the Russia-Ukraine Transit Agreement. This arrangement flows Russian gas via Ukraine to a few European countries, but was not renegotiated in large part due to the ongoing conflict between the two countries. However, markets had speculated early that the pipeline negotiations wouldn’t succeed, and reaction was limited as that speculation proved accurate.

Downward pressure came from Chinese importers reselling liquefied natural gas (LNG) cargoes and the Israel-Hamas ceasefire in January. Meanwhile, upward support came from colder temperatures, lowering gas storage levels, and Norwegian outages. In February, political risk grew as US tariffs on China and stalled tariffs on Mexico and Canada came together with other factors to drive a peak in pricing. The start of the decline came as peace talks to end the Russia/Ukraine war began. However, the talks have been complicated and are still ongoing – leaving an element of uncertainty over the future impact on the market.

In early March, US President Trump’s tariffs on goods from Canada and Mexico, plus increased tariffs on China, took effect. Those countries were quick to announce retaliatory tariffs, contributing to concerns about the US and Chinese economies, the re-emergence of higher inflation, and uncertainty around a potential ‘trade-war’. As it stands (in mid-March), the news about US tariffs is constantly changing and escalating, leaving the market vulnerable to further uncertainty.

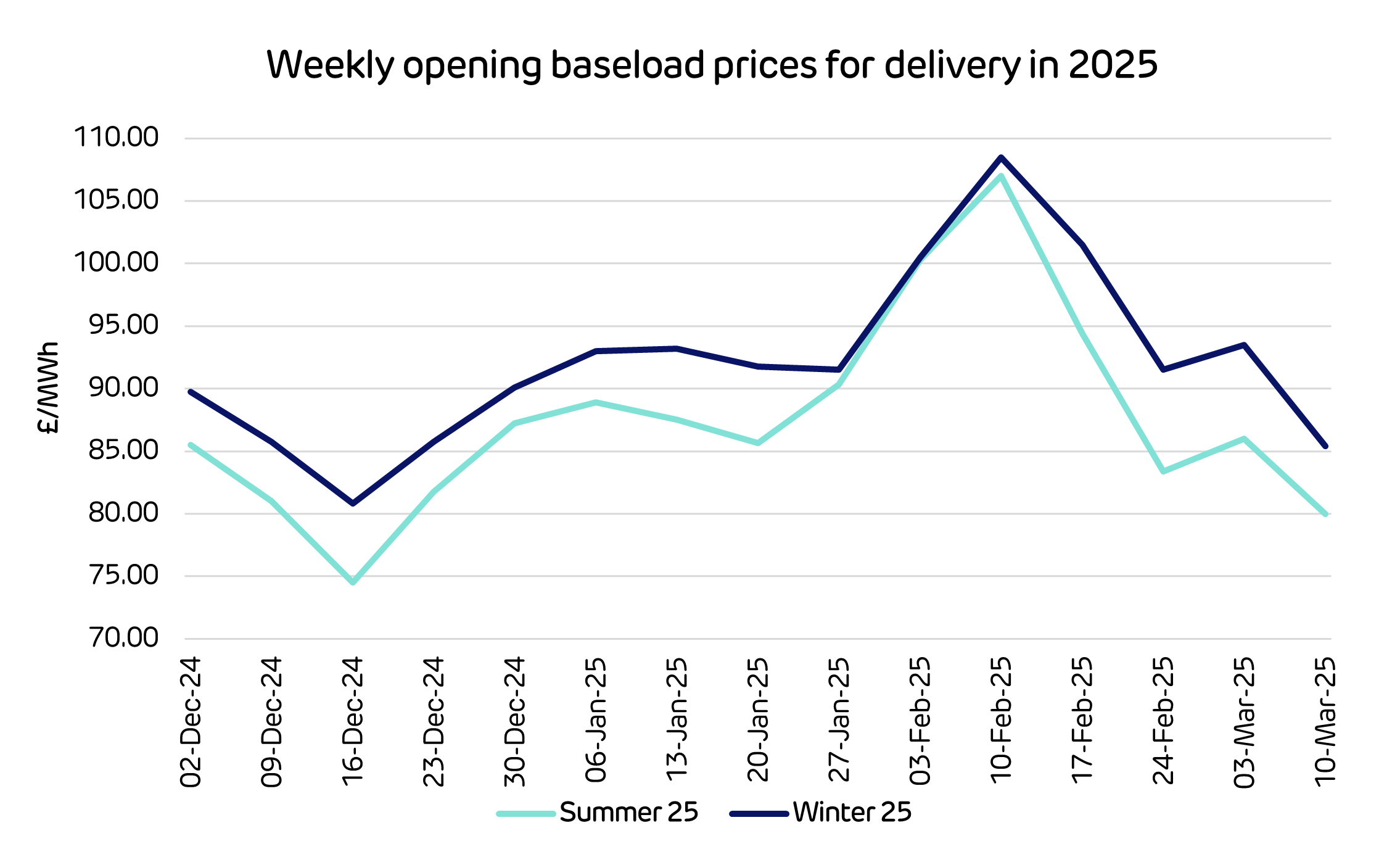

Looking at forward contracts for Summer and Winter 2025, we can see the market responding to similar drivers as those for the month-ahead contract.

The Winter 2025 premium over the Summer contract collapsed in early February, due to concerns about meeting European gas storage targets by November 2025. European gas storage levels are expected to trough at a lower point than the last two years. This is due to substantial withdrawals over the winter leading to greater gas-to-storage demand in the summer.

The potential for heightened European demand coinciding with Asian demand for heating added to the summer upward pressure. And an expected increase in LNG supply over the second half of 2025 lowered winter prices.

The Winter 2025 premium over the summer contract fell away sharply in late February. This occurred as several EU member states expressed a desire to lower storage targets, and the European Commission announced flexibility in meeting filling targets. Concurrently, Asian LNG demand dampened on higher prices and a milder-than-usual winter across much of North Asia.

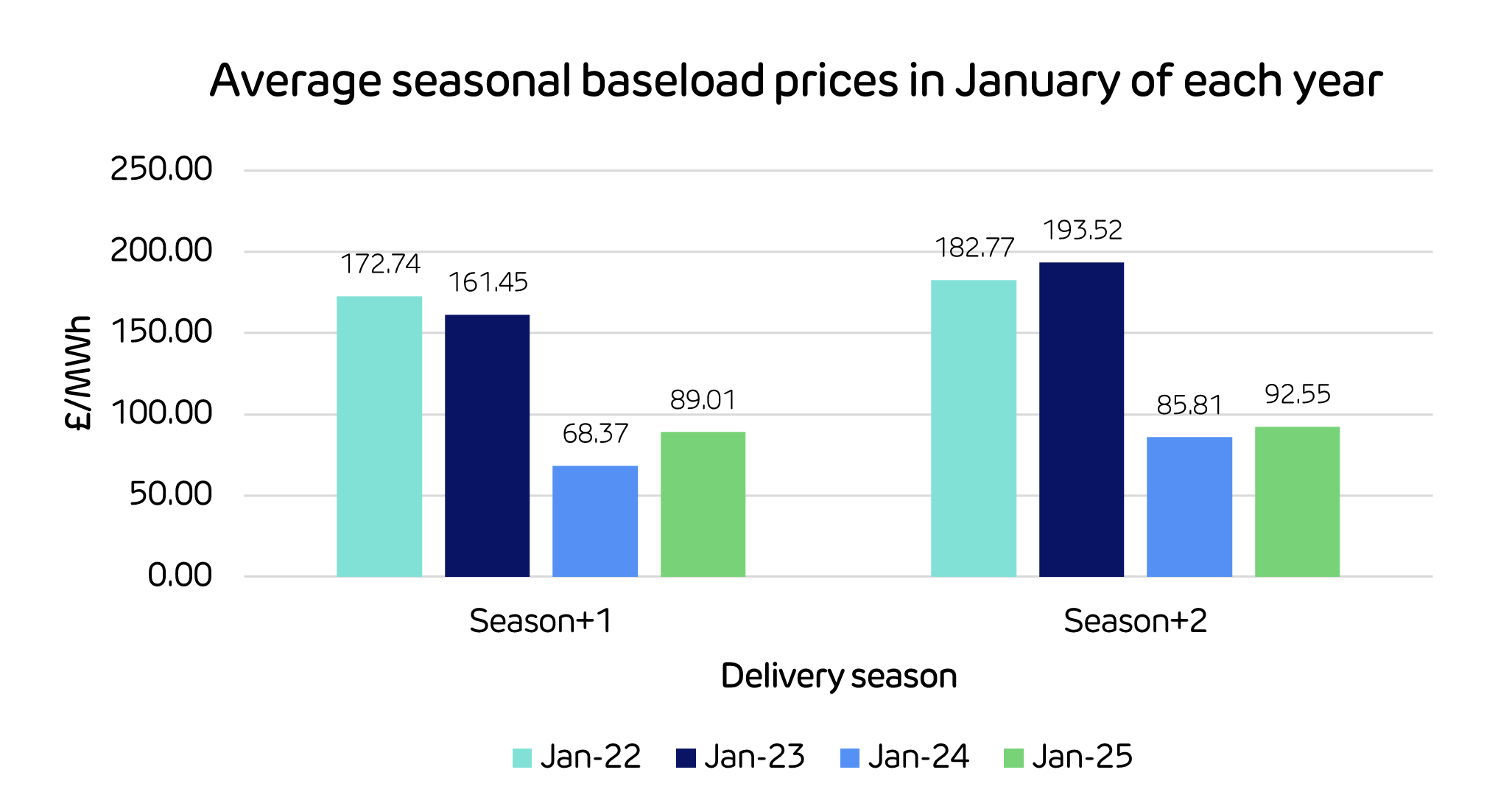

The following chart compares the average baseload price in January of each year for the summer and winter ahead. Prices have been lower over this winter and the previous winter. However, we can see the Summer-Winter spread was much more pronounced last year, as gas storage is much emptier this January than it was last year.

This reflects Europe’s adjustment to reduced gas flows from Russia, importing more Norwegian gas, and dramatically increasing LNG imports from the US and other global partners. With Covid, the Russian invasion of Ukraine, and political turmoil over the past couple of months, it’s difficult to identify a ‘normal’ benchmark.

Future outlook

In the past five years, volatility has become the ‘new normal’ with global events shaping the agenda. And the future of energy prices remains uncertain for similar reasons. There’s ongoing geopolitical and economic uncertainty, driven by the widespread escalation of trade tariffs by the world’s largest economy. Additionally, the Russia-Ukraine conflict and peace talks in the Middle East continue. What’s more, many of the drivers we’ve discussed will play an important part in price evolution. In particular, the progress of EU storage refilling and the availability of LNG cargoes, alongside any significant unplanned outages in Norway, will all affect prices.

Longer term drivers include the construction of LNG export facilities and the speed of transition away from fossil fuels by the world’s largest economies.

Global LNG Outlook estimates significant growth in LNG supply in 2025 to 2028 compared to the previous years. Much of this is expected to come from the US, which currently has five LNG projects under construction, in addition to Qatar, with the development of the North Field complex to boost liquefaction capacity. Additional LNG projects are being developed in Russia, Canada, and Africa.

The UK government’s plan for Clean Power 2030 will see more renewable generation on the system, offsetting gas consumption. However, to de-link gas and power prices, the market needs to reduce the number of hours in the year when gas is the marginal fuel. There’s more on this topic in our recent Electric Insights article.

Disclaimer

We’ve used all reasonable efforts to ensure that the content in this article is accurate, current, and complete at the date of publication. However, we make no express or implied representations or warranties regarding its accuracy, currency or completeness. We cannot accept any responsibility (to the extent permitted by law) for any loss arising directly or indirectly from the use of any content in this article, or any action taken in relying upon it.