Final transmission charges for 2026 almost identical to draft tariffs

On 30 January, the National Energy System Operator (NESO) issued the final Transmission Network Use of System (TNUoS) tariffs for the 2026-27 charging year. The fixed residual tariff, which comprises over 90% of the charge for consumers, is 0.75%-0.76% lower than the figure NESO shared in the draft tariff. While the final tariffs are almost identical to the draft tariffs, they’ll be significantly higher than those currently levied.

For context, April 2026 marks the start of the new five-year price control for electricity transmission (RIIO-ET3). We expected a large increase in TNUoS tariffs this year following Ofgem’s Draft Determinations in July 2025. Fundamentally, the electricity transmission network requires significant upgrades to its infrastructure to transport power from remote locations to population centres. NESO recovers this investment from users of the system, with consumers predominantly bearing the burden of any unallocated costs.

Comparison to 2025-26 tariffs

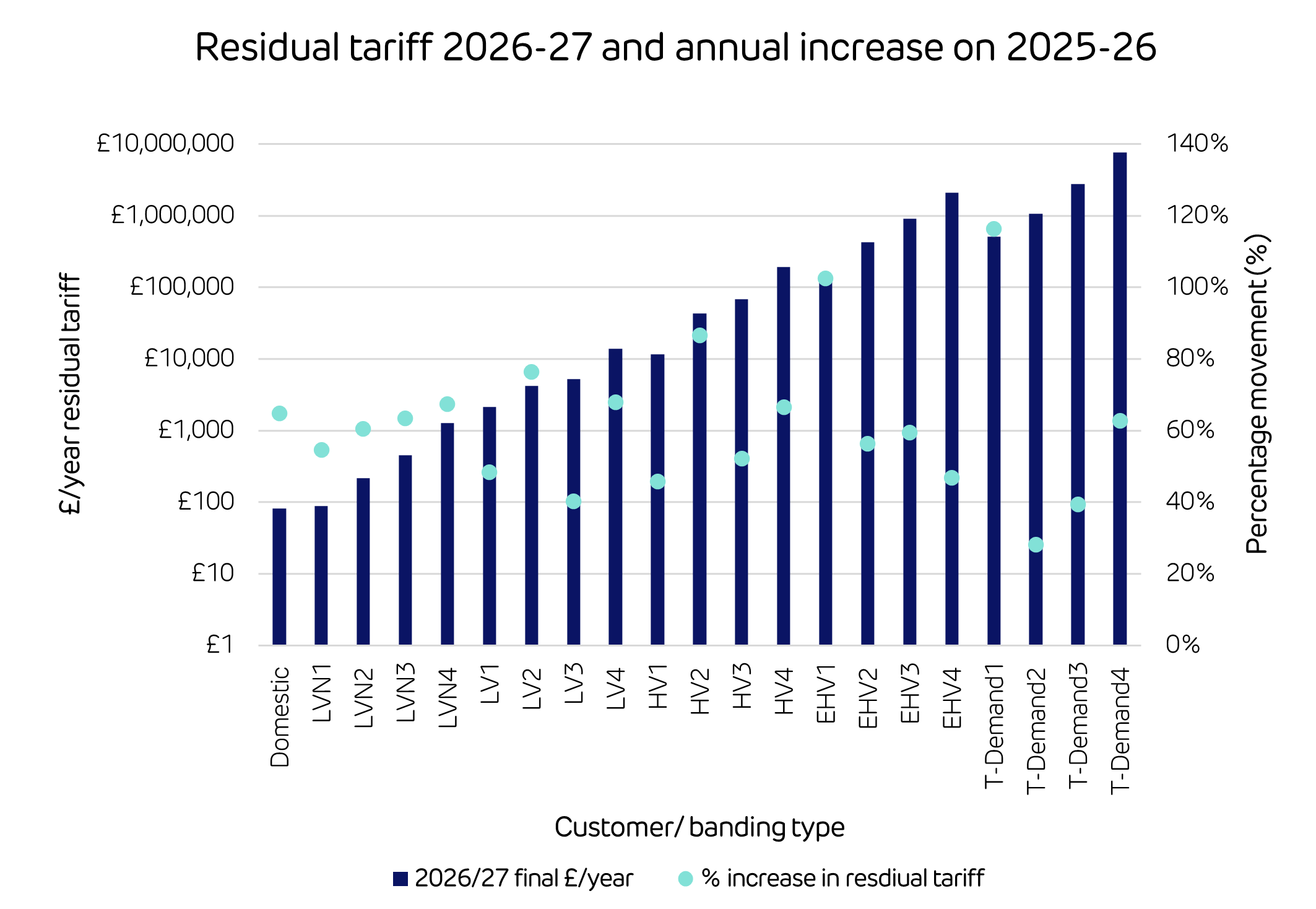

For most power consumers, the residual tariff represents over 90% of the total TNUoS cost in a year. These residual charges will increase by between 28% and 116% for power consumers in April, with a volume weighted average rise of 64% year-on-year. The following graph shows annual costs and percentage increases by consumer banding type.

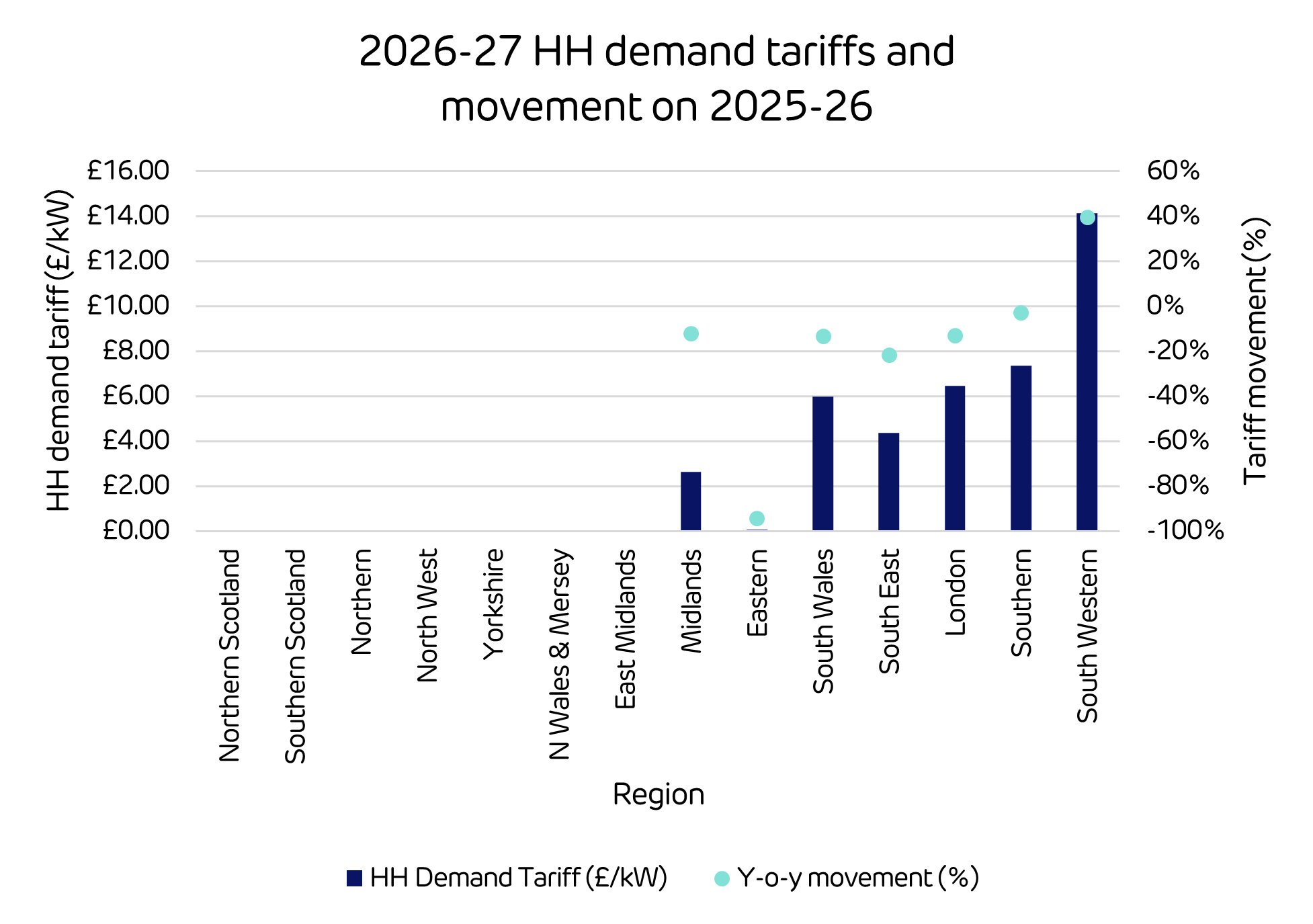

The so-called triad or demand half-hourly (HH) tariff is levied on consumption over the three half-hour periods of peak demand in the winter (with some caveats). There’s no triad tariff for those in the north of England and Scotland, and the tariff for those in the south has, predominantly, fallen. South Western is the only region seeing an increase from April, while the Eastern region’s tariff will be only £0.06/kW. This is displayed in more detail below.

A very similar trend exists for the non-half hourly (NHH) volumetric charge, which is levied on NHH consumption on weekdays, 4-7pm.

Comparison to draft tariffs

As we mentioned in the introduction, NESO’s final charges for both the residual fixed charge and the volumetric charges are very close to the draft tariffs issued in December.

Fixed charges are 0.75%-0.76% lower than those previously published, because total TNUoS revenues have fallen £44.87m since the draft tariff to £7.61bn.

Volumetric charges range from 4% lower (Midlands) to 1% higher (Eastern) than draft forecasts. NESO’s draft tariffs suggested the Eastern region would have no volumetric tariffs, but the finals show they do, albeit a near zero tariff. The movements are due to changes in nodal demand and embedded generation forecasts. NESO has also factored in the decisions from a recent modification to the charging rules (CMP463).

Residual banding to change – don’t be caught out!

The residual charging bands that determine what consumers pay is changing from 1 April 2026. So we’re advising customers to check these banding movements to better understand the potential impacts on their energy costs over the next five years.

2027-28 NESO TNUoS forecasts

NESO will issue its initial forecast of 2027-28 TNUoS tariffs in April 2026.

Disclaimer

We’ve used all reasonable efforts to ensure that the content in this article is accurate, current, and complete at the date of publication. However, we make no express or implied representations or warranties regarding its accuracy, currency or completeness. We cannot accept any responsibility (to the extent permitted by law) for any loss arising directly or indirectly from the use of any content in this article, or any action taken in relying upon it.

Subscribe to our newsletter

Sign up to our monthly newsletters and get the best of Drax Insights sent directly to your inbox.